production, theory of

economics

Introduction

in economics, an effort to explain the principles by which a business firm decides how much of each commodity that it sells (its “outputs” or “products”) it will produce, and how much of each kind of labour, raw material, fixed capital good, etc., that it employs (its “inputs” or “factors of production”) it will use. The theory involves some of the most fundamental principles of economics. These include the relationship between the prices of commodities and the prices (or wages or rents) of the productive factors used to produce them and also the relationships between the prices of commodities and productive factors, on the one hand, and the quantities of these commodities and productive factors that are produced or used, on the other.

The various decisions a business enterprise makes about its productive activities can be classified into three layers of increasing complexity. The first layer includes decisions about methods of producing a given quantity of the output in a plant of given size and equipment. It involves the problem of what is called short-run cost minimization. The second layer, including the determination of the most profitable quantities of products to produce in any given plant, deals with what is called short-run profit maximization. The third layer, concerning the determination of the most profitable size and equipment of plant, relates to what is called long-run profit maximization.

Minimization of short-run costs (cost)

The production function

However much of a commodity a business firm produces, it endeavours to produce it as cheaply as possible. Taking the quality of the product and the prices of the productive factors as given, which is the usual situation, the firm's task is to determine the cheapest combination of factors of production that can produce the desired output. This task is best understood in terms of what is called the production function, i.e., an equation that expresses the relationship between the quantities of factors employed and the amount of product obtained. It states the amount of product that can be obtained from each and every combination of factors. This relationship can be written mathematically as y = f (x1, x2, . . . , xn; k1, k2, . . . , km). Here, y denotes the quantity of output. The firm is presumed to use n variable factors of production; that is, factors like hourly paid production workers and raw materials, the quantities of which can be increased or decreased. In the formula the quantity of the first variable factor is denoted by x1 and so on. The firm is also presumed to use m fixed factors, or factors like fixed machinery, salaried staff, etc., the quantities of which cannot be varied readily or habitually. The available quantity of the first fixed factor is indicated in the formal by k1 and so on. The entire formula expresses the amount of output that results when specified quantities of factors are employed. It must be noted that though the quantities of the factors determine the quantity of output, the reverse is not true, and as a general rule there will be many combinations of productive factors that could be used to produce the same output. Finding the cheapest of these is the problem of cost minimization.

The cost of production is simply the sum of the costs of all of the various factors. It can be written:

in which p1 denotes the price of a unit of the first variable factor, r1 denotes the annual cost of owning and maintaining the first fixed factor, and so on. Here again one group of terms, the first, covers variable cost (roughly“direct costs” in accounting terminology), which can be changed readily; another group, the second, covers fixed cost (accountants' “overhead costs”), which includes items not easily varied. The discussion will deal first with variable cost.

The principles involved in selecting the cheapest combination of variable factors can be seen in terms of a simple example. If a firm manufactures gold necklace chains in such a way that there are only two variable factors, labour (specifically, goldsmith-hours) and gold wire, the production function for such a firm will be y = f (x1, x2; k), in which the symbol k is included simply as a reminder that the number of chains producible by x1 feet of gold wire and x2 goldsmith-hours depends on the amount of machinery and other fixed capital available. Since there are only two variable factors, this production function can be portrayed graphically in a figure known as an isoquant diagram (Figure 1-->). In the graph, goldsmith-hours per month are plotted horizontally and the number of feet of gold wire used per month vertically. Each of the curved lines, called an isoquant, will then represent a certain number of necklace chains produced. The data displayed show that 100 goldsmith-hours plus 900 feet of gold wire can produce 200 necklace chains. But there are other combinations of variable inputs that could also produce 200 necklace chains per month. If the goldsmiths work more carefully and slowly, they can produce 200 chains from 850 feet of wire; but to produce so many chains more goldsmith-hours will be required, perhaps 130. The isoquant labelled “200” shows all the combinations of the variable inputs that will just suffice to produce 200 chains. The other two isoquants shown are interpreted similarly. It is obvious that many more isoquants, in principle an infinite number, could also be drawn. This diagram is a graphic display of the relationships expressed in the production function.

The principles involved in selecting the cheapest combination of variable factors can be seen in terms of a simple example. If a firm manufactures gold necklace chains in such a way that there are only two variable factors, labour (specifically, goldsmith-hours) and gold wire, the production function for such a firm will be y = f (x1, x2; k), in which the symbol k is included simply as a reminder that the number of chains producible by x1 feet of gold wire and x2 goldsmith-hours depends on the amount of machinery and other fixed capital available. Since there are only two variable factors, this production function can be portrayed graphically in a figure known as an isoquant diagram (Figure 1-->). In the graph, goldsmith-hours per month are plotted horizontally and the number of feet of gold wire used per month vertically. Each of the curved lines, called an isoquant, will then represent a certain number of necklace chains produced. The data displayed show that 100 goldsmith-hours plus 900 feet of gold wire can produce 200 necklace chains. But there are other combinations of variable inputs that could also produce 200 necklace chains per month. If the goldsmiths work more carefully and slowly, they can produce 200 chains from 850 feet of wire; but to produce so many chains more goldsmith-hours will be required, perhaps 130. The isoquant labelled “200” shows all the combinations of the variable inputs that will just suffice to produce 200 chains. The other two isoquants shown are interpreted similarly. It is obvious that many more isoquants, in principle an infinite number, could also be drawn. This diagram is a graphic display of the relationships expressed in the production function.Substitution of factors

The isoquants also illustrate an important economic phenomenon: that of factor substitution. This means that one variable factor can be substituted for others; as a general rule a more lavish use of one variable factor will permit an unchanged amount of output to be produced with fewer units of some or all of the others. In the example above, labour was literally as good as gold and could be substituted for it. If it were not for factor substitution there would be no room for further decision after y, the number of chains to be produced, had been established.

The shape of the isoquants shown, for which there is a good deal of empirical support, is very important. In moving along any one isoquant, the more of one factor that is employed, the less of the other will be needed to maintain the stated output; this is the graphic representation of factor substitutability. But there is a corollary: the more of one factor that is employed, the less it will be possible to reduce the use of the other by using more of the first. This is the property known as “diminishing marginal rates of substitution.” The marginal rate of substitution of factor 1 for factor 2 is the number of units by which x1 can be reduced per unit increase in x, output remaining unchanged. In the diagram, if feet of gold wire are indicated by x1 and goldsmith-hours by x2, then the marginal rate of substitution is shown by the steepness (the negative of the slope) of the isoquant; and it will be seen that it diminishes steadily as x2 increases because it becomes harder and harder to economize on the use of gold simply by taking more care. The remainder of the analysis rests heavily on the assumption that diminishing marginal rates of substitution are characteristic of the production process generally.

The cost data and the technological data can now be brought together. The variable cost of using x1, x2 units of the factors of production is written p1x1 + p2x2, and this information can be added to the isoquant diagram (Figure 2-->). The straight line labelled v2, called the v2-isocost line, shows all the combinations of input that can be purchased for a specified variable cost, v2. The other two isocost lines shown are interpreted similarly. The general formula for an isocost line is p1x1 + p2x2 = v, in which v is some particular variable cost. The slope of an isocost line is found by dividing p2 by p1 and depends only on the ratio of the prices of the two factors.

The cost data and the technological data can now be brought together. The variable cost of using x1, x2 units of the factors of production is written p1x1 + p2x2, and this information can be added to the isoquant diagram (Figure 2-->). The straight line labelled v2, called the v2-isocost line, shows all the combinations of input that can be purchased for a specified variable cost, v2. The other two isocost lines shown are interpreted similarly. The general formula for an isocost line is p1x1 + p2x2 = v, in which v is some particular variable cost. The slope of an isocost line is found by dividing p2 by p1 and depends only on the ratio of the prices of the two factors.Three isocost lines are shown, corresponding to variable costs amounting to v1, v2, and v3. If 200 units are to be produced, expenditure of v1 on variable factors will not suffice since the v1-isocost line never reaches the isoquant for 200 units. An expenditure of v3 is more than sufficient; and v2 is the lowest variable cost for which 200 units can be produced. Thus v2 is found to be the minimum variable cost of producing 200 units (as v3 is of 300 units) and the coordinates of the point where the v2 isocost line touches the 200-unit isoquant are the quantities of the two factors that will be used when 200 units are to be produced and the prices of the two factors are in the ratio p2/p1. It may be noted that the cheapest combination for the production of any quantity will be found at the point at which the relevant isoquant is tangent to an isocost line. Thus, since the slope of an isoquant is given by the marginal rate of substitution, any firm trying to produce as cheaply as possible will always purchase or hire factors in quantities such that the marginal rate of substitution will equal the ratio of their prices.

The isoquant–isocost diagram (or the corresponding solution by the alternative means of the calculus) solves the short-run cost minimization problem by determining the least-cost combination of variable factors that can produce a given output in a given plant. The variable cost incurred when the least-cost combination of inputs is used in conjunction with a given outfit of fixed equipment is called the variable cost of that quantity of output and denoted VC(y). The total cost incurred, variable plus fixed, is the short-run cost of that output, denoted SRC(y). Clearly SRC(y) = VC(y) + R(K), in which the second term symbolizes the sum of the annual costs of the fixed factors available.

Marginal cost

Two other concepts now become important. The average variable cost, written AVC(y), is the variable cost per unit of output. Algebraically, AVC(y) = VC(y)/y. The marginal variable cost, or simply marginal cost 【MC(y)】 is, roughly, the increase in variable cost incurred when output is increased by one unit; i.e., MC(y) = VC(y + 1) - VC(y). Though for theoretical purposes a more precise definition can be obtained by regarding VC(y) as a continuous function of output, this is not necessary in the present case.

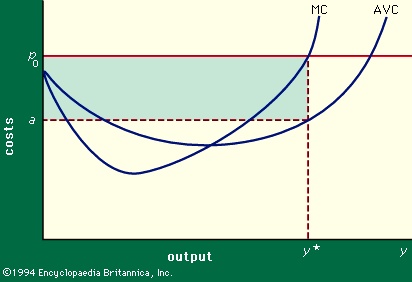

The usual behaviour of average and marginal variable costs in response to changes in the level of output from a given fixed plant is shown in Figure 3-->. In this figure costs (in dollars per unit) are measured vertically and output (in units per year) is shown horizontally. The figure is drawn for some particular fixed plant, and it can be seen that average costs are fairly high for very low levels of output relative to the size of the plant, largely because there is not enough work to keep a well-balanced work force fully occupied. People are either idle much of the time or shifting, expensively, from job to job. As output increases from a low level, average costs decline to a low plateau. But as the capacity of the plant is approached, the inefficiencies incident on plant congestion force average costs up quite rapidly. Overtime may be incurred, outmoded equipment and inexperienced hands may be called into use, there may not be time to take machinery off the line for routine maintenance; or minor breakdowns and delays may disrupt schedules seriously because of inadequate slack and reserves. Thus the AVC curve has the flat-bottomed U-shape shown. The MC curve, as might be expected, falls faster and rises more rapidly than the AVC curve.

The usual behaviour of average and marginal variable costs in response to changes in the level of output from a given fixed plant is shown in Figure 3-->. In this figure costs (in dollars per unit) are measured vertically and output (in units per year) is shown horizontally. The figure is drawn for some particular fixed plant, and it can be seen that average costs are fairly high for very low levels of output relative to the size of the plant, largely because there is not enough work to keep a well-balanced work force fully occupied. People are either idle much of the time or shifting, expensively, from job to job. As output increases from a low level, average costs decline to a low plateau. But as the capacity of the plant is approached, the inefficiencies incident on plant congestion force average costs up quite rapidly. Overtime may be incurred, outmoded equipment and inexperienced hands may be called into use, there may not be time to take machinery off the line for routine maintenance; or minor breakdowns and delays may disrupt schedules seriously because of inadequate slack and reserves. Thus the AVC curve has the flat-bottomed U-shape shown. The MC curve, as might be expected, falls faster and rises more rapidly than the AVC curve.Maximization of short-run profits

The average and marginal cost curves just deduced are the keys to the solution of the second-level problem, the determination of the most profitable level of output to produce in a given plant. The only additional datum needed is the price (price system) of the product, say p0.

The most profitable amount of output may be found by using these data. If the marginal cost of any given output (y) is less than the price, sales revenues will increase more than costs if output is increased by one unit (or even a few more); and profits will rise. Contrariwise, if the marginal cost is greater than the price, profits will be increased by cutting back output by at least one unit. It then follows that the output that maximizes profits is the one for which MC(y) = p0. This is the second basic finding: in response to any price the profit-maximizing firm will produce and offer the quantity for which the marginal cost equals that price.

Such a conclusion is shown in Figure 3-->. In response to the price, p0, shown, the firm will offer the quantity y* given by the value of y for which the ordinate of the MC curve equals the price. If a denotes the corresponding average variable cost, net revenue per unit will be equal to p0 - a, and the total excess of revenues over variable costs will be y*(p0 - a), which is represented graphically by the shaded rectangle in the figure.Marginal cost and price

The conclusion that marginal cost tends to equal price is important in that it shows how the quantity of output produced by a firm is influenced by the market price. If the market price is lower than the lowest point on the average variable cost curve, the firm will “cut its losses” by not producing anything. At any higher market price, the firm will produce the quantity for which marginal cost equals that price. Thus the quantity that the firm will produce in response to any price can be found in Figure 3--> by reading the marginal cost curve, and for this reason the marginal cost curve is said to be the short-run supply curve for the firm.The short-run supply curve for a product—that is, the total amount that all the firms producing it will produce in response to any market price—follows immediately, and is seen to be the sum of the short-run supply curves (or marginal cost curves, except when the price is below the bottoms of the average variable cost curves for some firms) of all the firms in the industry. This curve is of fundamental importance for economic analysis, for together with the demand curve for the product it determines the market price of the commodity and the amount that will be produced and purchased.

One pitfall must, however, be noted. In the demonstration of the supply curves for the firms, and hence of the industry, it was assumed that factor prices were fixed. Though this is fair enough for a single firm, the fact is that if all firms together attempt to increase their outputs in response to an increase in the price of the product, they are likely to bid up the prices of some or all of the factors of production that they use. In that event the product supply curve as calculated will overstate the increase in output that will be elicited by an increase in price. A more sophisticated type of supply curve, incorporating induced changes in factor prices, is therefore necessary. Such curves are discussed in the standard literature of this subject.

Marginal product

It is now possible to derive the relationship between product prices and factor prices, which is the basis of the theory of income distribution. To this end, the marginal product of a factor is defined as the amount that output would be increased if one more unit of the factor were employed, all other circumstances remaining the same. Algebraically, it may be expressed as the difference between the product of a given amount of the factor and the product when that factor is increased by an additional unit. Thus if MP1(x1) denotes the marginal product of factor 1 when x1 units are employed, then MP1(x1) = f(x1 + 1, x2, . . . ,xn; k) - f(x1, x2 . . . ,xn; k). The marginal products are closely related to the marginal rates of substitution previously defined. If an additional unit of factor 1 will increase output by f1 units, for example, then one more unit of output can be obtained by employing 1/f1 more units of factor 1. Similarly, if the marginal product of factor 2 is f2, then output will fall by one unit if the use of factor 2 is reduced by 1/f2 units. Thus output will remain unchanged, to a good approximation, if 1/f1 units of factor 1 are used to replace 1/f2 units of factor 2. The marginal rate of substitution is therefore f2/f1, or the ratio of the marginal products of the two factors. It has already been shown that the marginal rate of substitution also equals the ratio of the prices of the factors, and it therefore follows that the prices (or wages) of the factors are proportional to their marginal products.

This is one of the most significant theoretical findings in economics. To restate it briefly: factors of production are paid in proportion to their marginal products. This is not a question of social equity but merely a consequence of the efforts of businessmen to produce as cheaply as possible.

Further, the marginal products of the factors are closely related to marginal costs and, therefore, to product prices. For if one more unit of factor 1 is employed, output will be increased by MP1(x1) units and variable cost by p1; so the marginal cost of additional units produced will be p1/MP1(x1). Similarly, if additional output is obtained by employing an additional unit of factor 2, the marginal cost will be p2/MP2(x2). But, as shown above, these two numbers are the same; whichever factor i is used to increase output, the marginal cost will be pi/MPi(xi) and, furthermore, the firm will choose its output level so that the marginal cost will be equal to the price, p0.

Therefore it has been established that p1 = p0MP1(x1), p2 = p0MP2(x2), . . . , or the price of each factor is the price of the product multiplied by its marginal product, which is the value of its marginal product. This, also, is a fundamental theorem of income distribution and one of the most significant theorems in economics. Its logic can be perceived directly. If the equality is violated for any factor, the businessman can increase his profits either by hiring units of the factor or by laying them off until the equality is satisfied, and presumably the businessman will do so.

The theory of production decisions in the short run, as just outlined, leads to two conclusions (of fundamental importance throughout the field of economics) about the responses of business firms to the market prices of the commodities they produce and the factors of production they buy or hire: (1) the firm will produce the quantity of its product for which the marginal cost is equal to the market price and (2) it will purchase or hire factors of production in such quantities that the price of the commodity produced multiplied by the marginal product of the factor will be equal to the cost of a unit of the factor. The first explains the supply curves of the commodities produced in an economy. Though the conclusions were deduced within the context of a firm that uses two factors of production, they are clearly applicable in general.

Maximization of long-run profits

Relationship between the short run and the long run

The theory of long-run profit-maximizing behaviour rests on the short-run theory that has just been presented but is considerably more complex because of two features: (1) long-run cost curves, to be defined below, are more varied in shape than the corresponding short-run cost curves, and (2) the long-run behaviour of an industry cannot be deduced simply from the long-run behaviour of the firms in it because the roster of firms is subject to change. It is of the essence of long-run adjustments that they take place by the addition or dismantling of fixed productive capacity by both established firms and new or recently created firms.

At any one time an established firm with an existing plant will make its short-run decisions by comparing the ruling price of its commodity with cost curves corresponding to that plant. If the price is so high that the firm is operating on the rising leg of its short-run cost curve, its marginal costs will be high—higher than its average costs—and it will be enjoying operating profits, as shown in Figure 3-->. The firm will then consider whether it could increase its profits by enlarging its plant. The effect of plant enlargement is to reduce the variable cost of producing high levels of output by reducing the strain on limited production facilities, at the expense of increasing the level of fixed costs.In response to any level of output that it expects to continue for some time, the firm will desire and eventually acquire the fixed plant for which the short-run costs of that level of output are as low as possible. This leads to the concept of the long-run cost curve: the long-run costs of any level of output are the short-run costs of producing that output in the plant that makes those short-run costs as low as possible. These result from balancing the fixed costs entailed by any plant against the short-run costs of producing in that plant. The long-run costs of producing y are denoted by LRC(y). The average long-run cost of y is the long-run cost per unit of y 【algebraically LAC(y) = LRC(y)/y】. The marginal long-run cost is the increase in long-run cost resulting from an increase of one unit in the level of output. It represents a combination of short-run and long-run adjustments to a slight increase in the rate of output. It can be shown that the long-run marginal cost equals the marginal cost as previously defined when the cost-minimizing fixed plant is used.

Long-run cost curves

Cost curves appropriate for long-run analysis are more varied in shape than short-run cost curves and fall into three broad classes. In constant-cost industries, average cost is about the same at all levels of output except the very lowest. Constant costs prevail in manufacturing industries in which capacity is expanded by replicating facilities without changing the technique of production, as a cotton mill expands by increasing the number of spindles. In decreasing-cost industries, average cost declines as the rate of output grows, at least until the plant is large enough to supply an appreciable fraction of its market. Decreasing costs are characteristic of manufacturing in which heavy, automated machinery is economical for large volumes of output. Automobile and steel manufacturing are leading examples. Decreasing costs are inconsistent with competitive conditions, since they permit a few large firms to drive all smaller competitors out of business. Finally, in increasing-cost industries average costs rise with the volume of output generally because the firm cannot obtain additional fixed capacity that is as efficient as the plant it already has. The most important examples are agriculture and extractive industries.

Criticisms of the theory

The theory of production has been subject to much criticism. One objection is that the concept of the production function is not derived from observation or practice. Even the most sophisticated firms do not know the direct functional relationship between their basic raw inputs and their ultimate outputs. This objection can be got around by applying the recently developed techniques of linear programming, which employ observable data without recourse to the production function and lead to practically the same conclusions.

On another level the theory has been charged with excessive simplification. It assumes that there are no changes in the rest of the economy while individual firms and industries are making the adjustments described in the theory; it neglects changes in the technique of production; and it pays no attention to the risks and uncertainties that becloud all business decisions. These criticisms are especially damaging to the theory of long-run profit maximization. On still another level, critics of the theory maintain that businessmen are not always concerned with maximizing profits or minimizing costs.

Though all of the criticisms have merit, the simplified theory of production does nevertheless indicate some basic forces and tendencies operating in the economy. The theorems should be understood as conditions that the economy tends toward, rather than conditions that are always and instantaneously achieved. It is rare for them to be attained exactly, but it is just as rare for substantial violations of the theorems to endure.

Only the simplest aspects of the theory were described above. Without much difficulty it could be extended to cover firms that produce more than one product, as almost all firms do. With more difficulty it could be applied to firms whose decisions affect the prices at which they sell and buy (monopoly, monopolistic competition, monopsony). The behaviour of other firms that recognize the possibility that their competitors may retaliate (oligopoly) is still a theory of production subject to controversy and research.

Additional Reading

Authoritative intermediate-level discussions may be found in William J. Baumol, Economic Theory and Operations Analysis, 4th ed. (1977). Vernon L. Smith, Investment and Production (1961), especially emphasizes the relationship between long-run costs and investment. Probably the best technical presentation is Paul A. Samuelson, Foundations of Economic Analysis, enlarged ed. (1983). George J. Stigler, Production and Distribution Theories (1941, reissued 1994), provides a discussion of the evolution of the theory. J. Viner, “Cost Curves and Supply Curves,” Zeitschrift für Nationalökonomie, 3:23–46 (1931), remains a classic text. Ed.

- Colepeper, John Colepeper, 1st Baron

- Cole Porter

- Coleraine

- Coleridge, Hartley

- Coleridge, Samuel Taylor

- Coleridge, Sara

- Coleridge-Taylor, Samuel

- Coleroon River

- Cole, Sir Henry

- Cole, Thomas

- Colet, John

- Colet, Louise

- Colette

- Colette, Saint

- Coleus

- Colfax

- Colfax, Schuyler

- Colgate-Palmolive Company

- Colgate University

- colic

- coliform bacteria

- Coligny, Gaspard II de, Seigneur De Châtillon

- Colijn, Hendrikus

- Colima

- Colin Campbell, Baron Clyde (of Clydesdale)